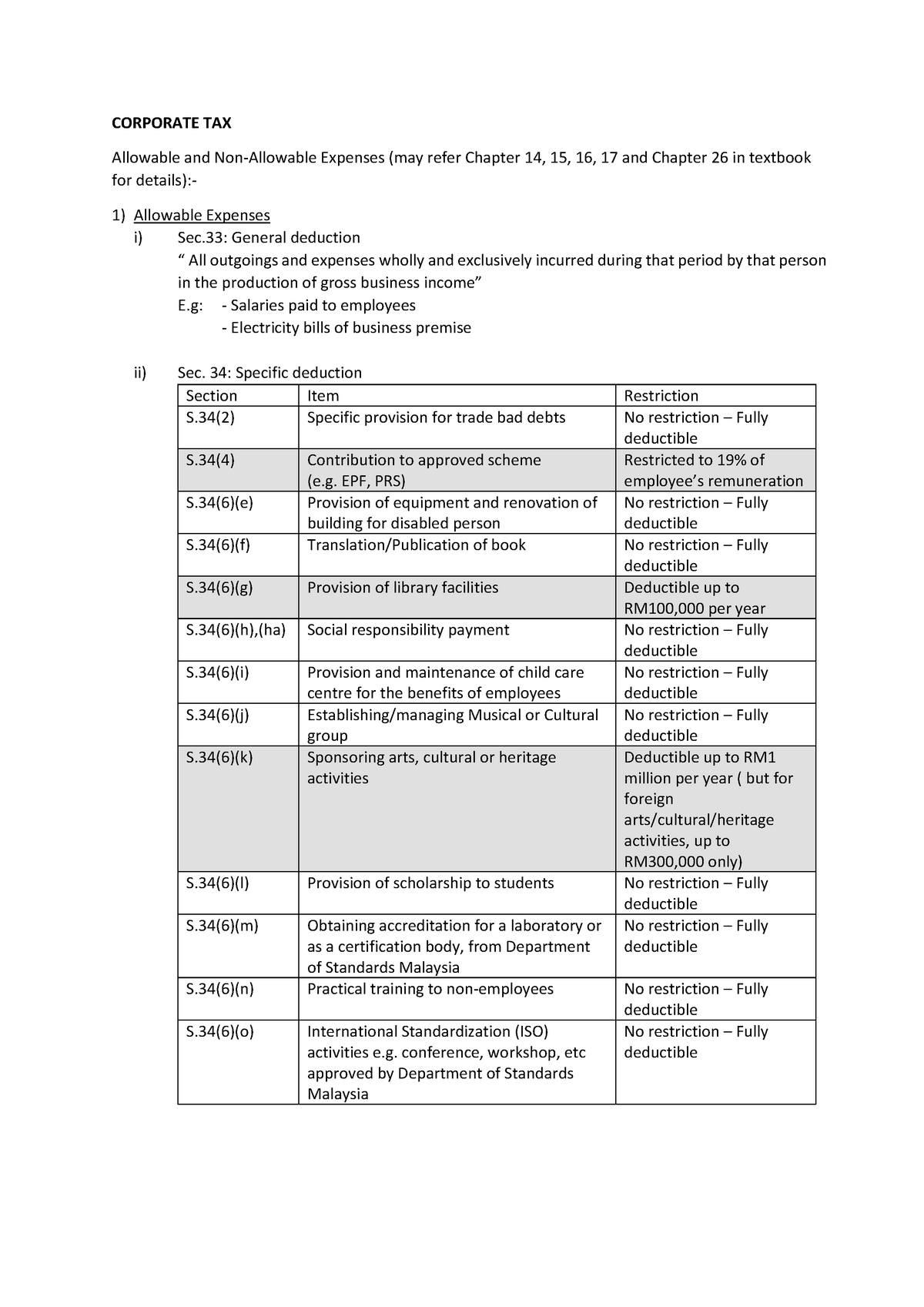

non allowable expenses for corporation tax malaysia

Active members attend club meetings have voting privileges may be elected as an officer of the club shall be counted towards a quorum of the club membership may participate in speech contests if they fulfill the other eligibility criteria and. International tax law distinguishes between an estate tax and an inheritance tax citation needed an estate tax is assessed on the assets of the deceased while an inheritance tax is.

Chapter 5 Corporate Tax Stds 2

An inheritance tax is a tax paid by a person who inherits money or property of a person who has died whereas an estate tax is a levy on the estate money and property of a person who has died.

. We are also able to handle any complex paper in any course as we have employed professional writers who are specialized in different fields of study. - Exemption from wharf dues export tax and import fees. The corporation tax filing and payment requirements and deadlines will be different.

If you are in the 396 percent tax bracket your capital gains tax rate will be 20 percent beginning in 2013. You can claim the following federal non-refundable tax credits that apply to you if you are reporting Canadian-source income. Andrew received P4000 dividend from a resident foreign P 24000 P 16000 corporation 60 of its historical income is from the 60 x P40000 40 x P40000 Philippines.

Central government HM Revenue Customs devolved governments and local governmentCentral government revenues come primarily from income tax National Insurance contributions value added tax corporation tax and fuel dutyLocal government revenues come. Entertainment and recreation expenses of a business are subject to a limit of 05 and 1 of net revenue for taxpayers engaged in selling goods and services respectively. Amortisation of goodwill is not deductible for tax purposes.

ASCII characters only characters found on a standard US keyboard. - A special tax rate of 5 of gross income in lieu of all national and local taxes after the income tax holiday. When assessing whether or not a given expense is deductible the first step is to see if the deduction is specifically prescribed by any clause of the Income Tax Act.

The government is implementing various support measures totaling B436 million 39 percent of GDP including i B25 million for health care ii B5 million for food programs iii B145 million for income support for job loss workers and self-employed iv B54 million to support business loans to SMEs with an additional B5 million. A group company that would otherwise qualify as an SME on a stand-alone basis is not eligible for SME benefits eg. Most often business entities are formed to sell a product or a service.

We offer assignment help in more than 80 courses. Taxation in the United Kingdom may involve payments to at least three different levels of government. 6 to 30 characters long.

In contrast it grew by 76 per cent in 2019 the largest recorded growth since 2007 while between 2012 and 2018 GDP grew 407 and key banking indicators like assets and credit exposures almost doubled. Most are deductible for income tax purposes. Reduced corporate tax rate preferable allowable ratios for deductible portion of bad debt provisions partial deductibility of entertainment expenses carryback of tax losses if the SME is owned by a parent company or two or.

Representation by Corporations Regarding Delinquent Tax Liability or a Felony Conviction under any Federal Law. There are many types of business entities defined in the legal systems of various countries. Non-deductible costs or payments are provided under Sections 40 and 40A.

In addition to the difference in the tax rates that apply the income tax rate is 20 and the corporation tax rate is 19 although increasing to 25 from 1 April 2023 there are other changes as a result of the move to corporation tax. In this situation interest expense on non-share equity would be treated as a dividend which is potentially frankable and would be non-deductible for the paying companygroup. This ensures all instructions have been followed and the work submitted is original and non-plagiarized.

Active Member An individual who is a paid member in good standing with Toastmasters International. We offer assignment help on any course. For mines depletion is allowable up to an amount not to exceed the market value as used for purposes of imposing the mining ad valorem taxes of the products mined and sold during the year.

The law allows companies to claim a deduction for interest expenses incurred in relation to offshore investments that generate non-assessable non-exempt dividend income. If you are in the 10-percent or 15-percent tax bracket then your capital gains tax rate is zero percent. The Armenian economy contracted sharply in 2020 by 57 mainly due to the 2020 Armenia-Azerbaijan war.

As noted in the Income determination section the UK tax system requires taxable profits to be calculated by aggregating i the companys net income from each source and ii the companys net chargeable gains arising from the sale of capital assetsThis approach gives rise to a particularly complicated regime so far as deductions are concerned. Provinces levy mining taxes on mineral extraction and royalties on oil and gas production. While part of the Soviet Union the economy of Armenia was based.

Government such as a non-immigrant visa may open and maintain bank accounts in the United States provided that the Cuban-national account holder may only. Corporation and P30000 dividend income from a non-resident foreign corporation. Must contain at least 4 different symbols.

- Income tax holiday of 4 to a maximum of 8 years for non-pioneer and pioneer projects respectively. Manufactures in the Philippines and sells to P 100000 P0 unaffiliated. Certification Regarding Tax Matters.

The maximum corporation tax deduction available under these rules for net borrowinginterest costs is limited to 30 of tax-adjusted EBITDA subject to some exceptions. Start-up expenses are deductible when incurred. Pursuant to 31 CFR 515571 Cuban nationals who are present in the United States in a non-immigrant status or pursuant to other non-immigrant travel authorization issued by the US.

Violation of Arms Control Treaties or Agreements - Certification. These include corporations cooperatives. While the default rate of the fixed ratio is set at 30 a taxpayer may in certain circumstances elect to deduct an amount in excess of 30 of tax-adjusted EBITDA under the.

Line 3 of Schedule B is less than 90. - Tax credit for import substitution. Browse our listings to find jobs in Germany for expats including jobs for English speakers or those in your native language.

In British Columbia a non-refundable 3 tax credit is available to qualifying corporations that develop natural gas and have an establishment in the province. A business entity is an entity that is formed and administered as per corporate law in order to engage in business activities charitable work or other activities allowable. Your allowable amount of provincial or territorial non-refundable tax credits if applicable is the amount on line 61500 of your provincial or territorial Form 428.

In addition a foreign corporation is subject to a 30 tax on the gross amount of certain US-source income not effectively connected with that business see section IIP1 below with respect to withholding on certain payments to non-US persons. Likewise interest expenses are not allowed as a tax expense if paid to a personal holding company that is more than 50 owned by a majority shareholder of the corporation. Reserve Officer Training Corps and Military Recruiting on Campus.

Such 30 tax potentially may be reduced or eliminated under an applicable US tax treaty. Glossary of Governing Documents. 37 can be used to determine if the expenditure is allowable.

Italy Commonwealth Fund

Japan Taxation Of Cross Border M A Kpmg Global

Where Should I Put My Savings Ubs United States Of America

R D Capital Allowances R D Capital Expenditure Explained

Tax Benefits Of Personal Goodwill In Mergers Acquisitions Transactions

Tax Treatment On Entertainment Expenses Asq

Tax Geek Tuesday Determining A Shareholder S Basis In S Corporation Stock And Debt

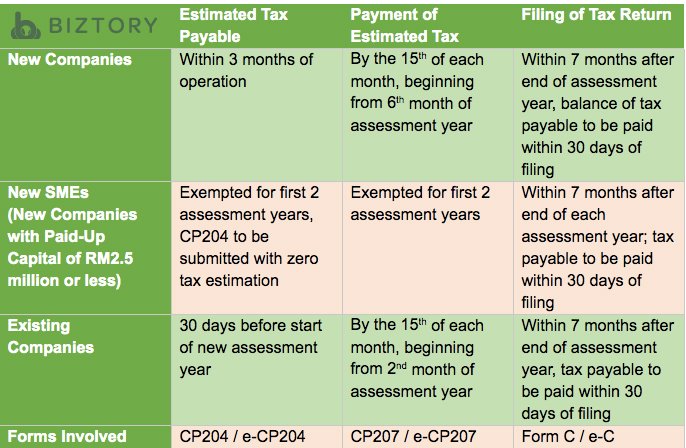

Corporate Tax Malaysia 2020 For Smes Comprehensive Guide Biztory Cloud Accounting

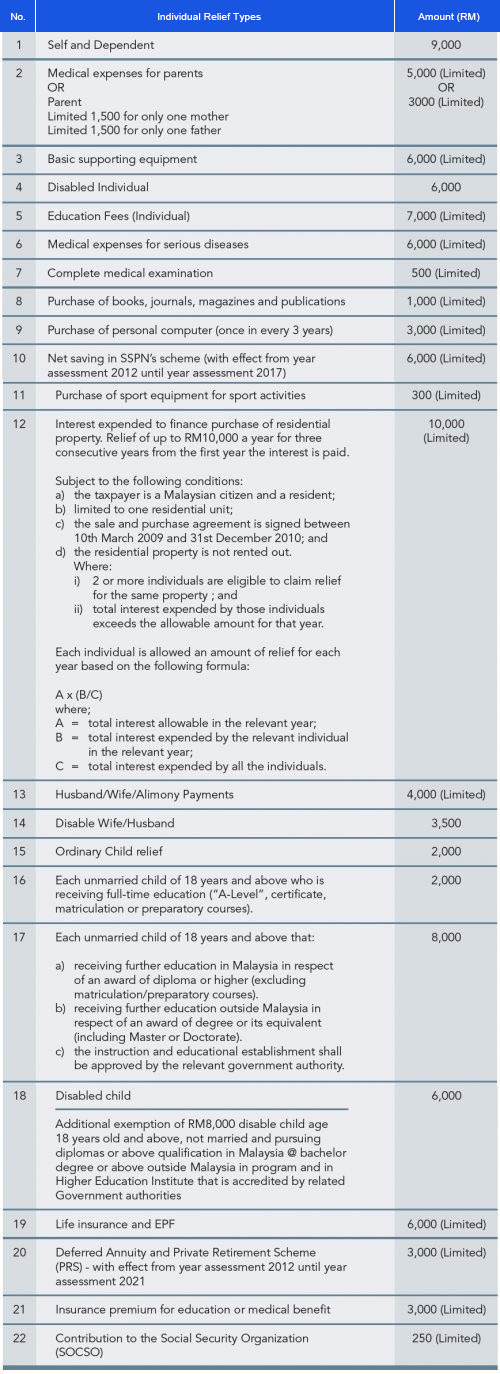

Understanding Tax Smeinfo Portal

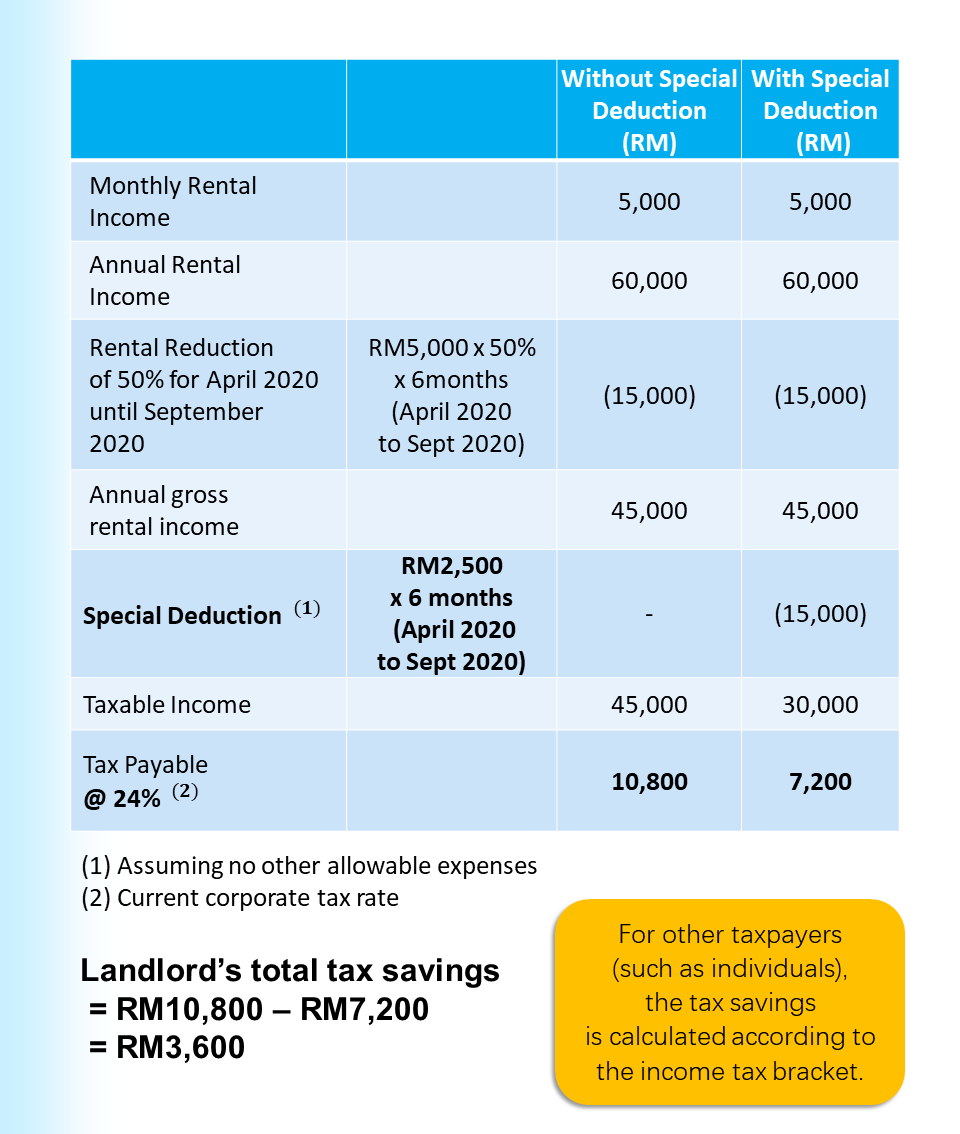

Special Tax Deduction On Rental Reduction

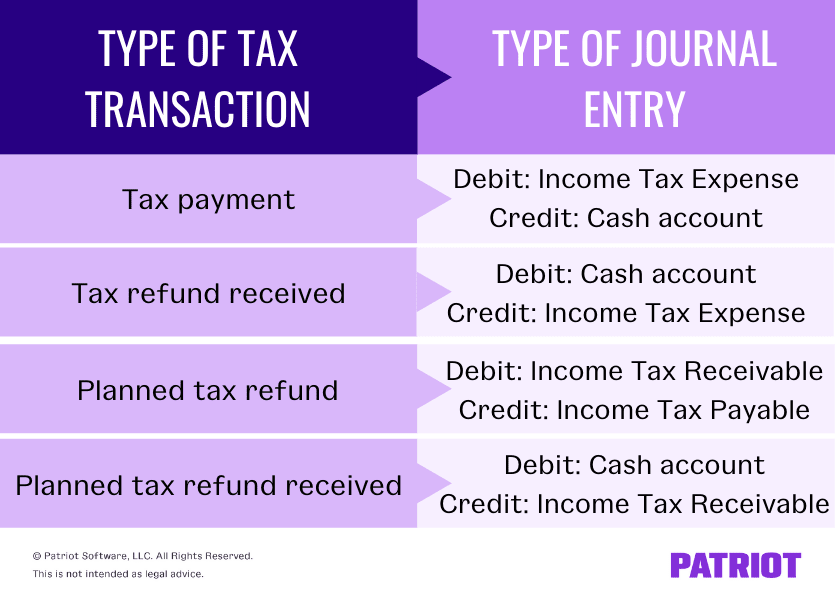

Journal Entry For Income Tax Refund How To Record In Your Books

Corporate Tax Note Tax317 Corporate Tax Allowable And Non Allowable Expenses May Refer Chapter Studocu

Japan Taxation Of International Executives Kpmg Global

Understanding Tax Smeinfo Portal

Irrevocable Trusts What Beneficiaries Need To Know To Optimize Their Resources J P Morgan Private Bank

15 Small Business Tax Tips To Legally Reduce Your Tax Bill 2022

Corporate Income Tax In Malaysia Acclime Malaysia

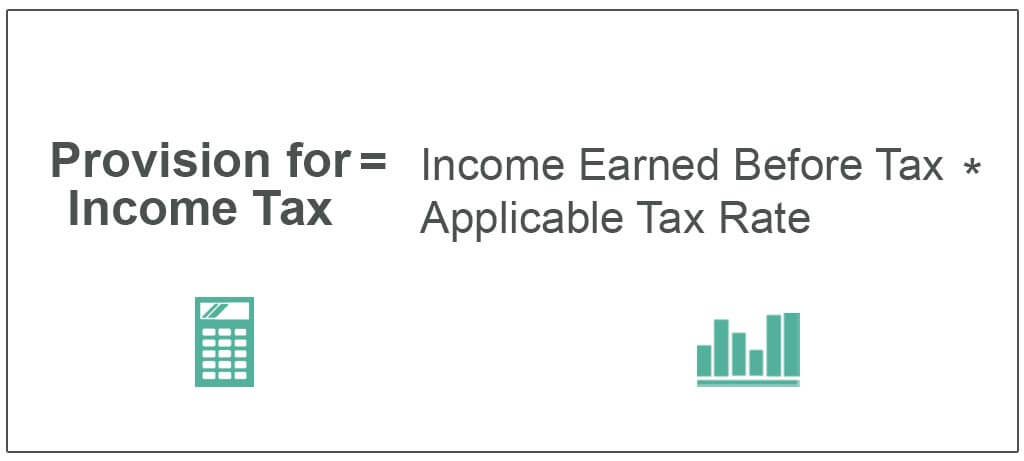

Provision For Income Tax Definition Formula Calculation Examples

This Is Principle Of Taxation Question Please I Need Chegg Com

0 Response to "non allowable expenses for corporation tax malaysia"

Post a Comment